IoT & Embedded Technology Blog

Why did Silicon Labs Acquire RTOS Vendor Micrium? Think IoT-focused MCUs.

Silicon Labs announced its acquisition of Micrium yesterday. While we had anticipated Micrium’s acquisition for quite some time, given the shrinking pool of commercial competitors in the MCU-targeted real-time operating system (RTOS) space, we were surprised to see Silicon Labs as the eventual acquirer, given how well Micrium could have integrated into various major IoT portfolios. In this blog we discuss why this acquisition makes sense from both companies’ perspectives, and how it will enable them to break out of their respective stagnating market segments.

Silicon Labs – Reaching for the MCU

Silicon Labs’ core business is “mixed-signal integrated circuits (ICs)…electronic components that convert real-world analog signals, such as sound and radio waves, into digital signals that electronic products can process” – a.k.a. sensors and digital signal processors (DSPs). Sensors and DSPs are less complex than the processors designed by companies such as Intel, ARM, Intel, NXP/Freescale, Renesas, etc. that end up inside of desktops, laptops, infotainment systems, and smartphones. Silicon Labs’ hardware tends to be integrated into less compute-intensive systems: smart lighting, wearables, industrial/automotive sensing, POS terminals, and routers are common examples.

Silicon Labs generated revenues of $645M in 2015, making it one of the smaller IC players relative to market leaders in the MCU/DSP space such as Texas Instruments ($8.3B in “Analog” revenues in 2015) and Analog Devices ($3.4B in total revenues in 2015). Unlike the largest silicon vendors, Silicon Labs does not own and operate any semiconductor fabricators. Instead, it creates proprietary IC designs in its facilities and then outsources the actual manufacturing of these chip and board blueprints to Asian fabrication giants Taiwan Semiconductor Manufacturing Co. (TSMC) and TSMC-affiliate Semiconductor Manufacturing International Corporation (SMIC).

In short, Silicon Labs is a smaller player whose future growth depends on the smart positioning and packaging of its custom ICs and MCUs. Its products are important components of connected devices, but they are relatively simple and commoditized; thus, the company must differentiate by layering and integrating the a comprehensive software portfolio on top of its hardware. After all, hardware is nothing without the software that tells it what to do. To this end, it must enable faster, easier MCU software development to add value to its IoT-targeted silicon which tends to be more software-rich than standard sensors and DSPs. Silicon Labs has already taken steps towards the IoT with its newer 32-bit ARM Cortex M0+/M3/M4 MCUs which will be sold into connected, (relatively) compute-intensive smart home and wearables applications.

Micrium – An IoT Enabler Remains Semi-Autonomous

Enter Micrium – a well-respected RTOS vendor formed in 1999 whose flagship OS, µC/OS, can be found in annual shipments of hundreds of millions of devices, generally at the MCU level and below. Although the company is among the most successful and widely-known commercial vendors in the space, pressure from free and/or open source competitors such as FreeRTOS and mbedOS have eroded its profits in recent years. Micrium recently introduced a free, maker version of µC/OS in an attempt to win mindshare with the cost-conscious maker market and combat free alternatives. Ultimately, Micrium hoped to convert these makers and startups to paid customers after helping them reach a certain size with its premium OS and tools. Many RTOS vendors have been forced to slowly transition away from comfortable commercial licensing model to a similar, lower-profit, hybrid model in recent years.

According to Brandon Lewis and Rich Nass of Embedded Computing Design, Micrium will continue to operate as a separate business under Silicon Lab’s IoT division. This structure is reminiscent of the early Intel/Wind River arrangement, and will allow Micrium to continue to support non-Silicon Labs hardware and architectures. Additionally, “the Micrium brand, offerings, and website will remain unchanged, and employment offers have been extended to all current Micrium staff.”

Now, with a parent organization to support it, Micrium will be able to focus less on costly marketing campaigns and business model reorganizations, and more on providing the best RTOS and tools possible for Silicon Labs’ customers, and MCU-class devices in general. Silicon Labs will greatly benefit from Micrium’s strong brand and solid RTOS line, helping it push upwards into the IoT MCU space with a compelling and respected OS to offer customers alongside its IC products. This acquisition will enable both to move towards a harmonized, IoT-focused MCU portfolio and break out of stagnating markets if handled correctly.

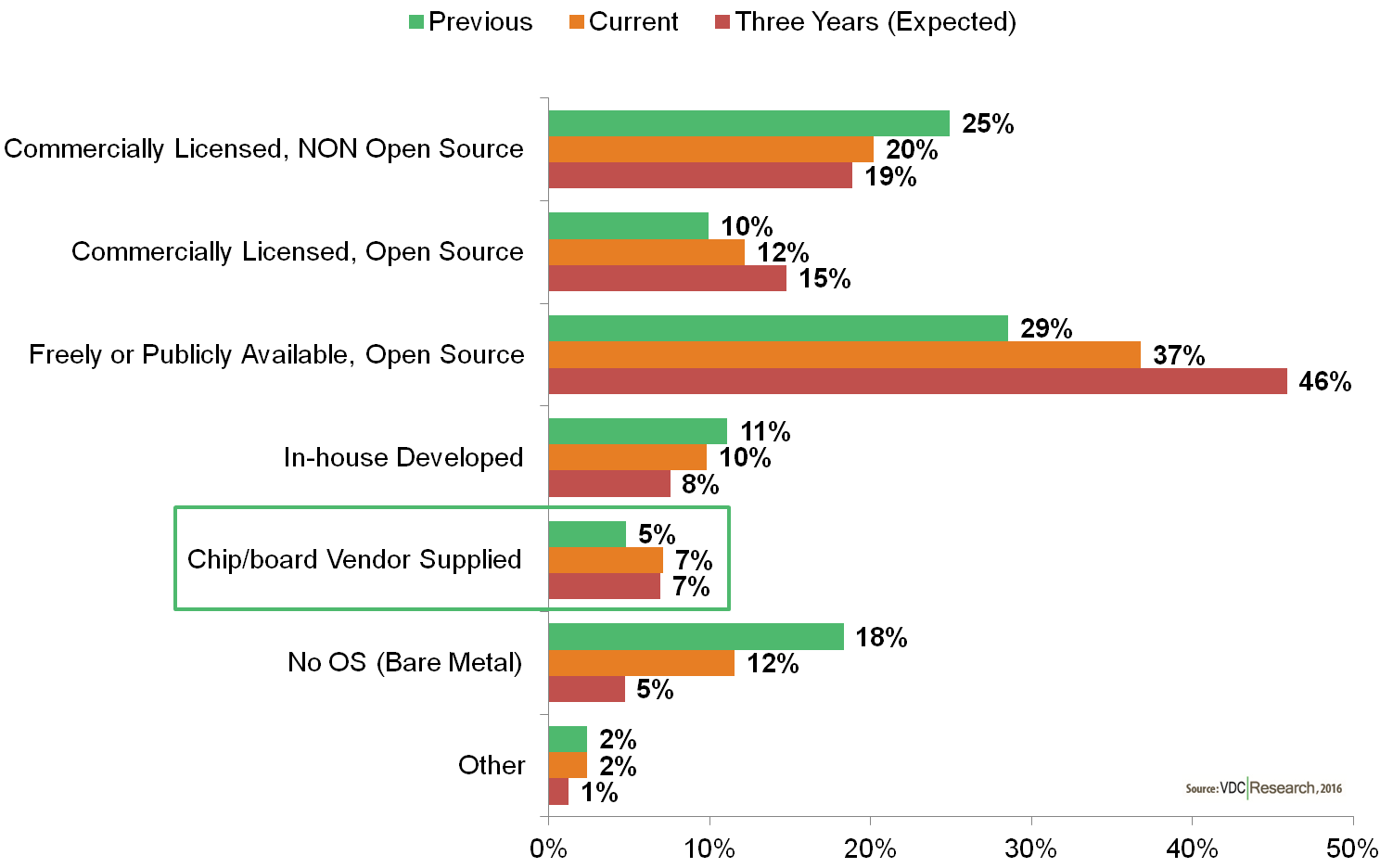

Exhibit 1: Previous, Current, and Expected Source of Primary Embedded Operating System

More Acquisitions on the Horizon from New Players

It is important to look at overall trends in the OS market in order to put this acquisition in context. Exhibit 1 shows interim findings from our 2016 embedded engineer survey. Only 7% of the engineers surveyed are currently using a chip/board vendor supplied OS, up slightly from 5% usage on the previous project. The real growth story is clearly around freely/publicly available, open source operating systems such as FreeRTOS (WITTENSTEIN), mbedOS (ARM), or Zephyr/Rocket (Wind River) in the MCU space where Micrium/Silicon Labs plays. As such, we expect to see the associated pricing, selling, and marketing pressures building to the point where many other OS vendors look toward acquisitions to exit a tightening market.

Traditionally, as with the Micrium acquisition, silicon/IP vendors have seen the most value in adding reliable, brand-name OSs and development tools to their portfolios: ARM (Keil), Cavium (MontaVista), and Intel (Wind River) are the most relevant acquisitions to consider. Going forward, we expect to see non-traditional IoT software and infrastructure platform vendors looking closely at the embedded OS space. A compelling OS offering could drive millions of device signups for IoT services platforms such as AWS IoT, Microsoft Azure, and GE Predix which derive recurring revenues from services rendered to an installed base of devices. Onboarding an OS offering would allow these players to potentially hook analytics and connectivity services into the billions of MCUs that are shipped yearly, bumping up services revenues substantially. We analyze and discuss similar topics alongside quantitative market sizing in our latest 2016 IoT & Embedded Operating Systems report.

We are excited to see what comes of this new partnership between Micrium and Silicon Labs, and will be keeping our eye out for similar acquisitions in the near future.