Enterprise Mobility & the Connected Worker Blog

Q4 2015 Rugged Mobile Hardware Market Overview

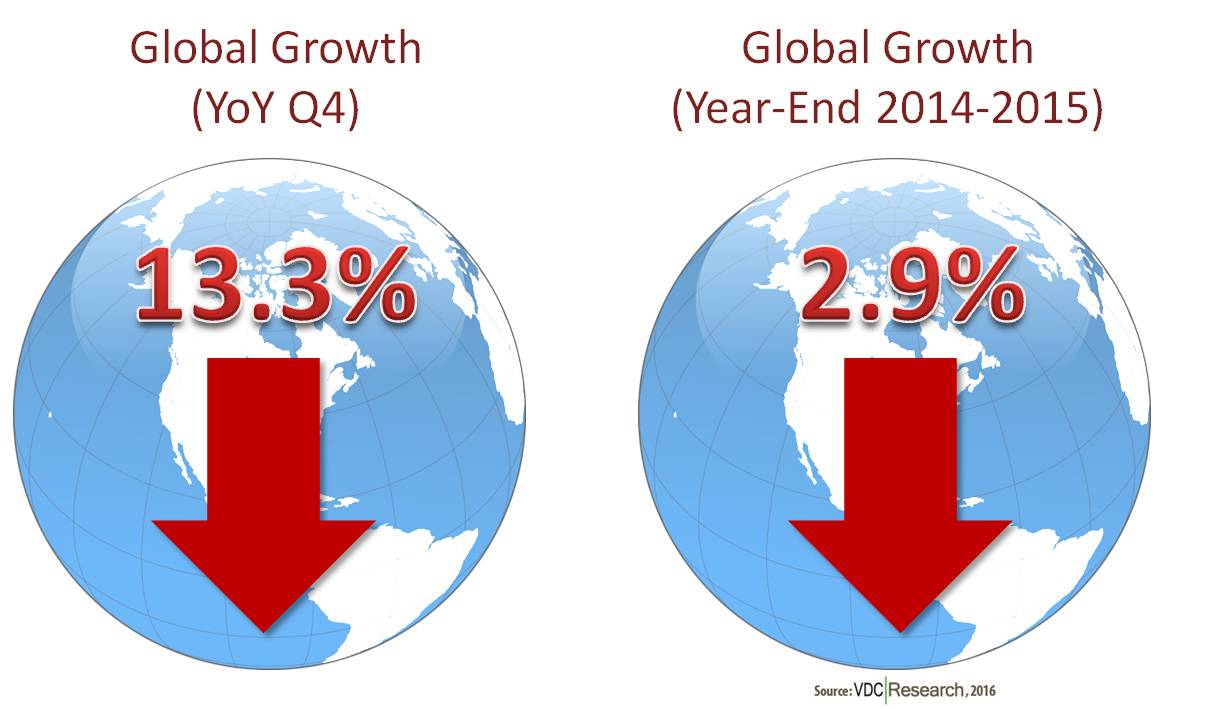

In Q4, the total rugged mobile hardware market, sized as all rugged notebooks, tablets, vehicle mounted devices, and handhelds, grossed just over $1.0 billion in revenue shipments and had over 1.1 million units ship. Looking at year-end data, the market grossed over $4 billion and shipped over 4.1 million units worldwide. The Q4 rugged market saw a year-over-year (YoY) revenue slide of 13.3% compared with its position in Q4 2014.

Figure 1: Rugged Mobile Hardware Global Overview

This $1+ billion per quarter market struggled in Q4, especially when compared to the quite strong Q4 of 2014. Looking at this YoY comparison, there was weakened global revenue shipments for rugged notebooks, tablets, handheld computing devices (the handhelds category includes devices such as smartphones and PDAs). As the past two quarters have been stymied by sluggish economic conditions in EMEA and low demand in the Americas, when looking at year-end total revenues for the rugged space, there was a slight overall contraction. Specifically, Figure 1 also shows that the total rugged device market shrank from 2014 to 2015 by 2.9%.

Breaking this weak Q4 2015 down by region we notice both the Americas and EMEA posted significant revenue losses in the handheld device space over Q4 2014, while APAC saw revenue stagnation over the same time period. However, it is important to note that when comparing 2014 year-end total revenue shipments to 2015’s data, both APAC and the Americas saw significant total growth in the handheld market. As Microsoft saw numerous slow-downs last year with their Windows 10 mobile enterprise release, their continued success in the mobile space hinges heavily on their evolving Azure Suite and eventual enterprise adoption (or lack thereof) of Windows 10 along with Continuum use. Overall, look for handhelds to have a difficult first half of the year in EMEA, but an okay first half in APAC and the Americas. The second half of the year looks far more promising for all regions for this form factor.

Tablets saw similar trends in Q4 2015 with EMEA and the Americas posting large revenue losses when compared to Q4 2014, but APAC actually saw just over 12% YoY growth over that same period. Looking at year-end total revenues, both EMEA and APAC saw YoY market growth, while the Americas market saw slight contraction, yielding slight overall market growth. The rugged tablet space currently faces increasing competition from consumer grade hardware vendors, especially in consumer facing roles such as in customer service. One possible area for growth within this space is the hybrid 2-in-1 tablet/notebook. With successes of consumer versions such as the Surface Pro and iPad Pro lines, the rugged opportunity for such devices could be leveraged in markets which would benefit from heavy text input capabilities of a physical keyboard coupled with the simple and efficient navigation of a tablet. Overall, we still expect to see tablet revenue growth this year, but it will be at a slower pace than previous years.

The rugged notebook space was hit hardest of all form factors both in comparing Q4 2015 to Q4 2014 and when comparing year-end totals from 2014 to 2015. In Q4, the rugged notebook market saw major YoY declines in both the Americas and APAC, with EMEA posting minor losses over the same time period. All regions witnessed between 15%-20% market contraction when comparing 2014 year-end total revenues to 2015 year-end total revenues. With vendors in this space retooling channels, sales strategies, and marketing over the later half 2015, this market should expect better performance than this especially weak Q4. While this change may not take immediate effect in Q1, definitely look for a stronger 2016 for rugged notebooks.

Overall, the rugged hardware market maintains a strong global presence; even in spite of weak fourth quarter revenue shipments and additional competition from consumer grade technologies. While this increased competition may prove a hindrance to traditional vendors in the rugged market space, it has forced many of these vendors to rethink traditional designs of devices. These additional research and development efforts are already bearing results, with recent product releases leveraging new ergonomic and design advances, often with specific vertical applications in mind. While these new releases have yet to impact bottom line revenues, the innovative thought and design behind being employed is undoubtedly having an effect on how vendors think about hardware design as well as end-user expectations in years to come. Additionally, as political and economic conditions continue to improve, especially in the EMEA regions, rugged revenues will likely increase compared to this past year.

View the 2017 Enterprise Mobility & Connected Devices Research Outline to learn more.