Enterprise Mobility & the Connected Worker Blog

Q3 2015 Rugged Mobile Hardware Market Overview

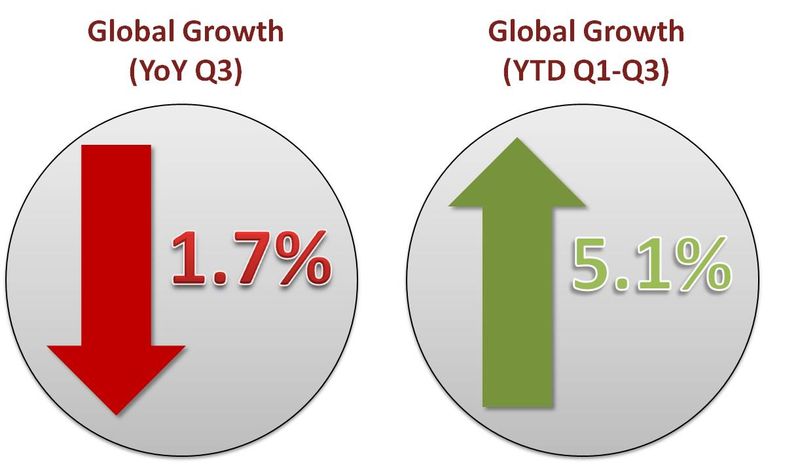

In Q3, the total rugged mobile hardware market, sized as all rugged notebooks, tablets, vehicle mounted devices, and handhelds, grossed just over $1 billion in revenue shipments and has produced year-to-date (YtD) revenue shipments of $3.2 billion. Also looking YtD, the market has shipped over 3.1 million units across the globe. By the end of Q4, we will likely see YtD revenue shipments surpass $4.2 billion and YtD unit shipments near 4.3 million units. While the rugged market has actually seen a year-over-year (YoY) revenue contraction of 1.7% compared with its position in Q3 2014, it has also produced 5.1% growth from Q1 2015 to Q3 2015.

Figure 1: Rugged Mobile Hardware Global Overview

Breaking down this $1 billion market by form factor, we find weakened global demand for rugged notebooks, stagnation in revenue for tablets, and strong revenue shipments for handheld devices (the handhelds category includes devices such as smartphones and PDAs). As economic conditions continue to stabilize, this recent growth comes as welcome news to many hardware vendors who look to take advantage of increased economic stability and opportunities presented in the Americas and Asia-Pacific (APAC) regions. For example, the growth in the handheld revenues occurred primarily in the Americas and APAC, with global YoY growth of 5.0% over Q3 2014.

While global tablet revenues shipments remained at similar levels to Q3 2014, EMEA generated more revenue shipments from tablets than from notebooks this quarter. One possible reason for this stagnation in growth is due to the increased competition from consumer grade tablets. One specific instance can be seen with the latest Microsoft Surface Pro, which has received relatively positive reviews and adoption from the enterprise market. Furthermore, both EMEA and APAC regions saw slight YoY growth in tablet revenues as the Americas saw minor YoY contraction. Rugged notebook revenues witnessed their highest quarterly performance on the year, but still had YoY revenue shipments fall in all regions, producing a global revenue dip of 14.9% between Q3 2014 to Q3 2015.

Overall, the rugged hardware market continues to maintain a strong global presence, even in spite of some areas of weakness and additional competition from consumer grade technologies. While this increased competition from consumer grade devices may seem like a hard hit to the rugged space, it can be counteracted with rugged vendors offering more advanced technological portfolios. Increases in processing speed, RAM, memory, camera quality, dual-OS capabilities, touch capacity, and enhanced security are all features which are slowly making their way from the consumer market into the rugged market space. As rugged vendors add these, and other, new technological facets to their mobile solutions, their specifications comparisons to consumer grade devices become far more attractive. Additionally, as economic conditions continue to improve, especially in the EMEA regions, rugged revenues will likely rebound for many form factors.

View the 2017 Enterprise Mobility & Connected Devices Research Outline to learn more.